Carl Zeiss 2023/q1

Carl Zeiss Meditec AG is one of the world’s leading medical technology companies, and it offers products and workflow solutions for the diagnosis and treatment of eye diseases. By providing innovations, equipment and network, the company not only enhance the workflows and doctors’ capabilities, but also improves the patients’ quality of life.

Carl Zeiss is an international company headquartered in Jena, Germany, and it has additional subsidiaries around the globe. It is listed in the MDAX and TecDAX on the German Stock Exchange.

The company as we know today, was created from a merger of the ZEISS Ophthalmology division with a medical lasers specialist Asclepion-Meditec AG, in 2002. But this recent merger should not mislead you on the expertise, knowledge and deep rooted history of the company. Carl Zeiss opened the very first workshop for precision mechanics and optics in 1846. Twenty years later, microsurgery on finest tissues began with Carl Zeiss surgical microscopes. Then in 1912, the department for medical optics and ophthalmology was founded. There are many such as milestones in the company’s history. All in all, emerging today to a world leader in ophthalmology and microsurgery did not come in a one day, but it builded on continues progress, innovations and developments. As of 31 March, the company had 4.624 employees.

Following this brief introduction, let me cover the financials of the company for 2023/q1.

But before that keep in mind, Carl Zeiss uses a fiscal calendar for its reports, which has a three month lag compared to January 1st of any year. Therefore 2023/q1 means here in this context, the first six months of fiscal year 2022/23.

1 – Segments and Regions

Carl Zeiss Meditec Group essentially has two main activity areas, and these areas also called as Strategic Business Units (SBU). The division of the strategic business units is based on the fields of application and customer groups within ophthalmology and microsurgery. Therefore, a distinction is made between the Ophthalmic Devices (OPT) SBU and Microsurgery (MCS) SBU.

When it comes to regions, Carl Zeiss reports its revenues under three categories: EMEA (Europe, Middle East, and Africa), Americas, and APAC (The Asia – Pacific). In Figure 1, I have presented both the recent quarter’s and last twelve months’ figures in million euros. On the upper side of the table, there are two segments and relevant revenues take place. From middle to the bottom side you can see the division of revenues based on the regions. Besides, I have added a quarter on quarter and year on year comparisons for the changes in these figures.

In Figure 2, you see net sales by these segments and regions. On the left side, pie chart shows us the two segments’ shares. At the end of first quarter, in 2023, revenues of Carl Zeiss stood at €504.2 million and “Ophthalmology” is the top line item with its 76% share in revenue. “Microsurgery” covers the rest with 24% and value is €119.9 million. On the right hand side of Figure 2, bars shows us that €248.5 million (50.3%) of the revenue comes from the APAC region. Americas and EMEA share the rest almost equally.

2 – Income Statement

A slowdown in global growth due to war in Ukraine, cost of living crisis and supply chain bottlenecks was not good for the profitability. On top of that Chinese market growth cast doubt on the future projections. Even under these conditions, Carl Zeiss managed to increase its revenue by a double-digit growth. Revenue has increased from €855.4 million to €974.5 million (13.9%) in the first six months of fiscal year 2022/23.

In order to follow the progress in the usual calendar, I have rearranged the data, and in Figure 3 you can see respectively in columns: the results of the first quarter of last year, last quarter and recent quarter. Upper side of the table examines the quarterly figures, and below is again LTM data.

Highlights from the Income Statement

Revenues have increased 7.2% compared to previous quarter and 13.3% compared to same quarter of the last year. Therefore, we can think that above mentioned negative effects did not cause much trouble. However, revenue is only the beginning. Because on the second and third rows we see that Cost of Sales, which has increased drastically, in YoY terms. That has reflected in the Gross Profit and end-result is shrinking EBIT margins. Although cost measures show their contribution at the quarterly changes YoY and LTM figures point out the squeeze in the operational profitability. I think that might be the reason behind the recent sell-off.

In Figure 4, I have reflected the last two columns data in a chart for those who prefer visual outputs to numbers. If we start with the striking minus 18.7% EBIT figure, it is the change compared to previous year’s same quarter and it obviously comes from the 20% increase in the cost of sales, which deteriorated the profitability. If we continue with the black bars, revenues increased 13.3% YoY and gross profit increased 8.8% at the same period.

In Figure 4, blue bars represent the quarterly changes. Again EBIT was incredibly strong with 38% jump. This is also related to cost controls at the first quarter of the year. Cost of sales decreased QoQ, and increase in the revenues positively effected the gross profit.

In Figure 5, you can follow changes on profit margins for a broader time span. As you can see from the quarterly data, Carl Zeiss has a solid, lucrative gross profit margin around 60%. However, EBIT margin fluctuates between 10 to 20 percent. Recent EBIT margin is 16.6%.

And for those who wonder the trend for revenues, cost of sales and gross profit, I have added quarterly data in Figure 6. The company has a stable revenue growth and costs seems to be under control. But one should also consider the ongoing investments and high operating expensed which are related to that, too. Gross profit at the end of first quarter of 2023 was €292.2 million.

In Figure 7, I have presented the components and a breakdown of Income Statement for the first quarter of 2023. Both higher selling and marketing expenses associated with the scheduled rollout of new products and the expansion of the company’s sales presence in the North American market brought a 25.2% increase in the costs. Meanwhile, Selling and Marketing Expenses also hit €101.9 million, General Administrative Expenses amounted to €22.5 million. Due to investments in digitalisation, Research and Development Expenses reached to €84.2 million, too.

As it can be followed from the above Sankey Diagram Operating Income was €83.6 million and after taxes paid, Net Income dropped to €63.3 million. In the end, consolidated profit that is attributable to shareholders of the parent company was €62.0 million and profit/loss attributable to non-controlling interests was €1.3 million.

3 – DCF Valuation

Discounted Cash Flows & Intrinsic Value

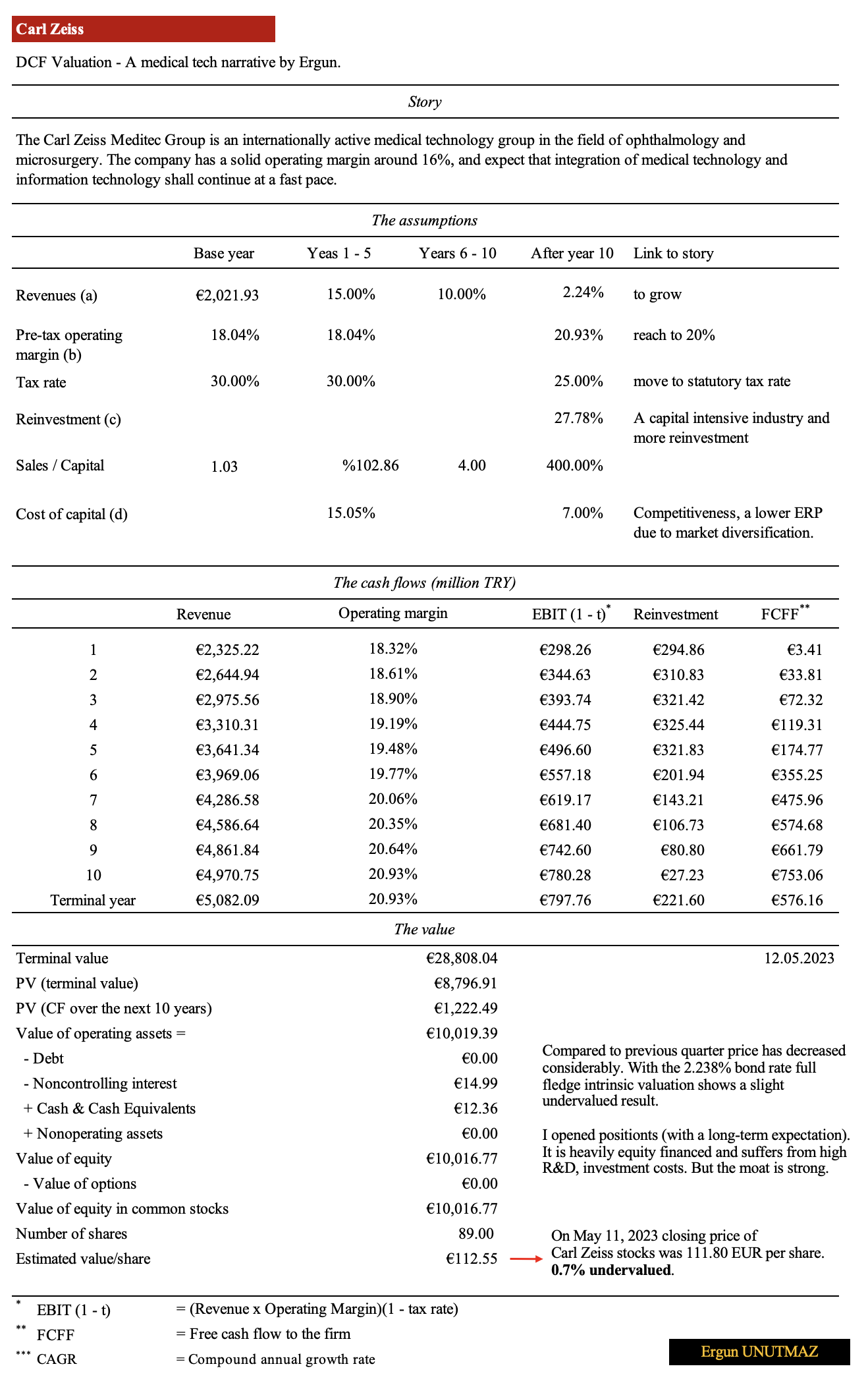

Carl Zeiss Meditec AG has solid gross profit margin and a strong moat in its business. Due to expertise, specialisation and high investment costs I expect this competitive advantage to prevail in the long term. As I have stated above, the operating costs are also too high, and EBIT margin suffers from the fluctuations in the markets. Even under these circumstances ten years of backward data and future guidance let me to take 20.9% pre-tax operating margin for the company. I also kept revenue growth in conservative terms and expect cost of capital to fall in steady state. In this study, I have used the current 10 year government bonds for Germany as a risk-free rate and it was 2,238% on May 11, 2023.

Below you can find the inputs and output of my recent DCF Valuation that reflects the 2023/Q1 results.

Discounted Cash Flows (DCF) Analysis

On May 11, 2023 closing price for the AFX stocks was 111.80 EUR per share. The intrinsic value that I have calculated was 112.55 EUR per share. According to my assumptions and expectations Carl Zeiss stocks was 0,7% undervalued.

Although analysts suggest 150.00 EUR per share value (and I do believe that potential) due to conservative choices I have made, my calculations did not match those estimates here in this quarter. Even though the stock is not heavily undervalued, I have started to add shares to my long-term investment portfolio. But I’d like to remind that all calculations are prone to error and even if they are perfect, markets have their own dynamics and value-price gap may widen before it converges.

4 – Fundamentals and Technical Analysis

Carl Zeiss has solid financial ratios. The company relies on equity finance than building a debt pile. Debt-to-Equtiy ratio in this regard was 0.38 at the end of 2023/q1. This in return keeps the Financial Leverage also at 0.28 and Total Liabilities (€754,1) make less than one third of the Total Assets (€2.732,1). When it comes to Current Ratio it stood at 3.43, which is considered to be high, but it might provide extra muscle for new opportunities. Quick Ratio was also at 2.53 and following a similar declining trend, which is also above the accepted limits.

You can check the 5 year trend for Financial Ratios in Figure 9.

Carl Zeiss share was listed on the German Stock Exchange on 22 July 2002 for the very first time. In its 20 years of being listed, the company has grown from an initial market capitalization of under €300 million to over €10 billion. In Figure 10, I have reflected the comparative returns of the Carl Zeiss Meditec AG (black) and DAX Index (blue). As you can see, the performance is dazzling.

If we focus our lenses to the las five year period, we can see from Figure 11 that Carl Zeiss had an upward and strong performance. On 13th September 2021, the stock price hit the €199.10 as the highest value and since then we are witnessing a fall. After diverging from the moving averages, shares did a tough correction. Since the beginning of 2022 there is a consolidation structure around €105.25 as a base.

I have attended the latest conference call on 09 May 2023 and the management’s presentation with a future guidance was convincing enough for me. There are obstacles ahead and due to geopolitic, macroeconomic and supply side problems this quarter may also turn out not so promising. However in the long-run the company may reach its goals. One last thought; loosing fifty percent of market capitalization always requires asking further questions. If there is a development, which didn’t reflect to financials yet, it might be disturbing and price might continue to dive under long term averages. But if this is not the case, then there might be an opportunity here. In either way, it’s up to you.

Ergun UNUTMAZ, 17.05.2023

You can read my previous works on similar subjects by clicking the links.

ŞİŞECAM Valuation 2023/q1

ŞİŞECAM Outlook 2022/q4

Şirket Analiz: Puma SE (PUM)

I wish you all the best.

Disclaimer

General information and statistics that are provided herein this article acquired from official sites and public resources. Thoughts and comments belong to the author and do not represent any other third parties’, public/private institutions’ or organisations’ point of view.

The information contained on this article is not an offer to buy or sell securities, foreign exchanges, indices or any other financial instruments. Works on this blog also comprise educational materials, translations, summaries and experience sharing essays. I do not provide any kind of financial services. For the investment advices and recommendations, please refer to registered institutions and authorised bodies. Parties, who gets information from this website, accept to bear the possible benefits and risks at their own responsibility, and act through their own initiative.

2 Comments

Minard

I admire your piece of work, regards for all the useful posts.

Ergun UNUTMAZ

Thanks